How Social Security is calculated determines how much you receive each month in retirement. Your benefit is based on your lifetime earnings, adjusted for inflation, and your claiming age.

Understanding the calculation formula — including AIME, PIA, and full retirement age — helps you estimate your real monthly benefit and avoid costly mistakes.

Step 1: Your Earnings History

The Social Security Administration reviews your highest 35 years of earnings. Each year is adjusted for inflation to reflect today’s wage levels.

Step 2: Calculate AIME (Average Indexed Monthly Earnings)

Your top 35 inflation-adjusted earning years are averaged and divided into a monthly number. This creates your AIME.

AIME Formula:

Total indexed earnings ÷ 420 months = Average Indexed Monthly Earnings

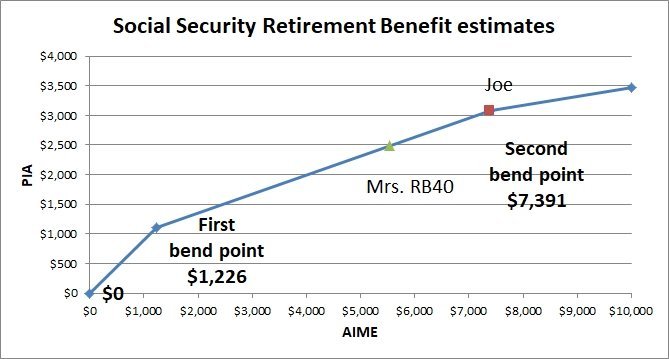

Step 3: Calculate PIA (Primary Insurance Amount)

Your PIA is calculated using a progressive formula with bend points. This ensures lower-income earners receive a higher percentage of their earnings.

Your PIA represents the benefit you receive at full retirement age.

Step 4: Adjust for Claiming Age

Claim at 62

Permanent reduction up to ~30%.

Full Retirement Age

Receive 100% of your calculated PIA.

Delay to 70

Increase benefit up to 24–32%.

See the full comparison here: Social Security benefits by age

Example Calculation

Example:

- AIME: $5,000

- PIA at FRA: $2,000

- Claim at 62: ~$1,400

- Claim at 70: ~$2,480

Final Thoughts

Understanding how Social Security is calculated gives you control over your retirement income. Before making a decision, confirm your full retirement age and compare claiming strategies carefully.